Home Storage Gold IRA — Why It Is Not Allowed

A home storage Gold IRA sounds simple, but the IRS says no. In McNulty v. Commissioner (2021), a taxpayer lost over $270,000 in taxes and penalties for keeping IRA gold in a home safe. One wrong storage decision can turn a tax-deferred account into a fully taxable distribution. This article covers the law, the court cases, the LLC scheme that failed, and the legal alternatives.

Key Takeaways

- IRS rules require Gold IRA metals to be held by a qualified trustee or approved depository — not in your home.

- Breaking this rule triggers income tax on the full account value plus a 10% penalty if you are under 59½.

- The LLC “loophole” has been rejected by the U.S. Tax Court and does not provide legal protection.

Can You Store Gold IRA Metals at Home?

No. The IRS does not allow it. Under 26 U.S. Code Section 408(m)(3)(B), precious metals held in an IRA must be in the physical possession of a bank, an approved non-bank trustee, or a depository that meets specific federal standards. Your home safe, a safety deposit box you rent personally, or a vault in your garage does not qualify.

This rule is not new or ambiguous. It has been part of the tax code since 1997, when Congress expanded the types of precious metals eligible for IRAs through the Taxpayer Relief Act. The same legislation that opened the door to gold in IRAs also closed the door to home storage. The two rules are inseparable.

Think of it like a driver's license: the government allows you to operate a vehicle, but only under specific conditions. You can hold gold in an IRA, but only if a qualified custodian maintains control. Remove the custodian from the equation, and you lose the tax-advantaged status entirely.

Why Does the IRS Prohibit Home Storage?

The prohibition rests on two legal concepts: the qualified trustee requirement and the doctrine of constructive receipt. Together, they make home storage of IRA metals a prohibited transaction under federal tax law.

The Qualified Trustee Requirement

Section 408(a) of the Internal Revenue Code requires that IRA assets be held by a trustee that is either a bank, a federally insured credit union, or an entity approved by the IRS under Section 408(n). Individual taxpayers do not qualify as trustees for their own retirement accounts. This is a structural requirement, not a guideline. It applies to all IRA assets, including precious metals (Source: 26 U.S. Code Section 408).

Constructive Receipt

Constructive receipt is a tax doctrine that says you do not need to physically cash a check to owe taxes on it. If you have unrestricted access to the funds, the IRS considers them distributed. Storing IRA metals in your home safe gives you unrestricted access to those assets. From the IRS perspective, that is no different from taking a cash distribution and putting the money under your mattress (Source: IRS Publication 590-B).

The constructive receipt doctrine is what makes home storage especially dangerous. Even if you never sell the metals, never spend the proceeds, and intend to return them to a depository later, the IRS treats the moment of personal possession as a taxable event. Intent does not matter. Physical access does.

What Happens If You Store IRA Gold at Home?

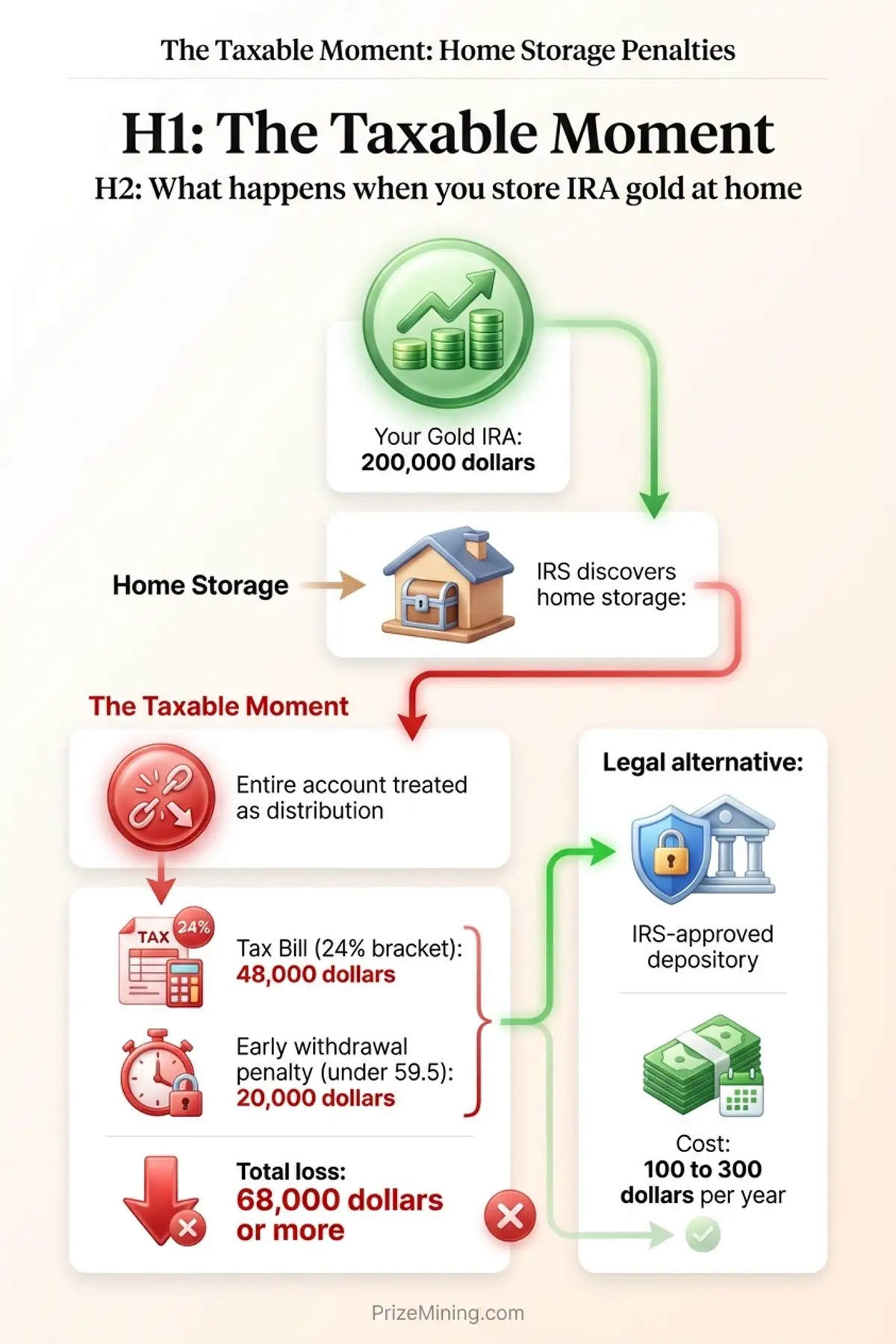

We call it “The Taxable Moment” because the damage happens at a single point in time: the instant you take personal possession of IRA-owned metals. At that moment, the IRS treats the entire account value as a distribution. Not just the metals you removed — the full balance.

Here is what the math looks like on a $200,000 Gold IRA for someone in the 24% federal tax bracket who is under 59 and a half.

| Item | Amount |

|---|---|

| IRA account value | $200,000 |

| Federal income tax (24%) | $48,000 |

| Early withdrawal penalty (10%) | $20,000 |

| State income tax (estimated 5%) | $10,000 |

| Total cost of The Taxable Moment | $78,000 |

That is 39% of the account gone in a single tax year. You still have the gold, but you have lost the tax-deferred wrapper that made the IRA valuable in the first place. And if the distribution pushes you into a higher bracket, the actual percentage could be even worse (Source: IRS Publication 590-B).

This is not a hypothetical scenario. In McNulty v. Commissioner (2021), a taxpayer used an LLC structure to store IRA metals at home. The U.S. Tax Court ruled the arrangement constituted a taxable distribution. The resulting tax bill on the $730,000 account exceeded $270,000, including penalties and interest. The court found no legal basis for treating the LLC as a qualified trustee (Source: McNulty v. Commissioner, T.C. Memo. 2021-37).

For a full picture of how Gold IRA tax rules govern distributions, penalties, and reporting requirements, see our dedicated tax rules page.

Does the LLC Loophole Actually Work?

Setting up an LLC to hold your own IRA gold is like writing yourself a prescription — the structure may look official, but it violates the rules. Several companies sell a structure they call a “checkbook IRA” or “home storage IRA LLC.” The pitch sounds sophisticated: your self-directed IRA creates a limited liability company, the LLC opens a bank account, the LLC buys precious metals, and you store those metals in a home safe that the LLC technically “owns.” The argument is that the LLC, not you personally, holds the metals, so the trustee requirement is satisfied.

Here is how the scheme works step by step.

- Step 1: You open a self-directed IRA with a custodian that permits alternative investments.

- Step 2: Your IRA invests its funds into a newly formed LLC, with you as the manager.

- Step 3: The LLC opens a checking account and uses IRA funds to purchase gold or silver.

- Step 4: The metals are delivered to your home, stored in a safe you purchased for the LLC.

- Step 5: The promoter claims this is legal because the LLC, not you, holds the metals.

The U.S. Tax Court has rejected this argument. In McNulty v. Commissioner, the court found that the taxpayer's physical access to and control over the metals constituted constructive receipt, regardless of the LLC intermediary. The LLC did not change who had access to the gold. The taxpayer could walk to the safe and remove the coins at any time. That access made it a distribution (Source: McNulty v. Commissioner, T.C. Memo. 2021-37).

When we first encountered companies marketing LLC home storage structures in 2024, the legal arguments looked plausible on the surface. After reading the full Tax Court opinion and consulting the IRS code sections cited in the ruling, we concluded that the LLC adds a layer of paperwork without adding a layer of legal protection. The IRS looks through the entity to the person who controls the assets. An LLC where you are the sole manager and the metals sit in your basement does not satisfy the qualified trustee requirement.

The analogy is straightforward: putting your car title in an LLC does not change who drives the car. The IRS applies the same logic to precious metals. If you control the assets, you have received them for tax purposes.

Companies that promote this structure often charge $1,500 to $5,000 for the LLC setup, plus ongoing annual fees for the entity. You pay thousands of dollars for a structure the Tax Court has already struck down. Our Gold IRA scams page covers this and other deceptive practices in the industry (Source: Yahoo Finance).

Home Storage IRA vs Owning Gold at Home

This distinction confuses many investors, and the confusion is not accidental. Companies selling home storage IRA setups blur the line between two very different things. One is illegal. The other is perfectly fine.

| Factor | Home Storage Gold IRA | Owning Gold at Home |

|---|---|---|

| Funding source | Pre-tax IRA dollars | After-tax personal funds |

| IRS rules apply | Yes — full IRA regulations | No IRA rules — standard property |

| Storage location | Must be approved depository | Anywhere you choose |

| Tax consequence of home storage | Full distribution + 10% penalty | None — already taxed |

| Legal status | Prohibited transaction | Completely legal |

If you want to hold physical gold in your home, the legal path is simple: buy it with money you have already paid taxes on. You can purchase coins, bars, or rounds from any reputable dealer, store them however you like, and sell them whenever you choose. You will owe capital gains tax when you sell at a profit, but there are no penalties, no custodian requirements, and no trustee rules.

The distinction is like the difference between renting a car through your company and owning a car personally. The company car comes with rules about who can drive it, where you can park it, and how you report the mileage. Your personal car has none of those restrictions. IRA gold is the company car. Personal gold is yours to do with as you please (Source: US News).

For a complete walkthrough of how the custodian and depository relationship works in a properly structured account, see our how a Gold IRA works page.

What Are the Legal Storage Options?

If home storage is off the table, where do Gold IRA metals actually go? A depository for your Gold IRA works like a parking garage with full insurance — your property stays secure and the facility is liable if anything goes wrong. The answer is an IRS-approved depository — a specialized vault facility that meets federal security, insurance, and reporting standards. Two storage models are available, and the choice affects both cost and how your metals are handled.

Segregated Storage

In segregated storage, your specific coins and bars are kept in a separate container or vault section, physically isolated from other investors' holdings. When you take a distribution or sell, you receive the exact items you purchased. Segregated storage typically costs $150 to $300 per year, depending on the depository and the value of metals stored.

Commingled Storage

In commingled (or allocated-but-pooled) storage, your metals are stored alongside those of other investors. The depository tracks your ownership by weight, type, and purity, but your specific bars or coins are not isolated. When you take a distribution, you receive equivalent items, not necessarily the exact ones you purchased. Commingled storage usually costs $100 to $150 per year (Source: LendEDU).

Which Should You Choose?

Segregated storage costs more but provides certainty: you get back the same serial-numbered bars or specific coins you bought. Some investors prefer this for estate planning or simply for peace of mind. Commingled storage saves money each year and works well for standard bullion products where one bar is functionally identical to another.

Both options are fully legal and satisfy the IRS custodian requirement. The major depositories serving the Gold IRA industry, including Delaware Depository and Brink's Global Services, offer both options. Your custodian may have a preferred depository relationship, which can limit your choices. Ask about depository options before opening an account.

Storage fees are one layer of the overall cost structure. Our Gold IRA risks page covers how fees, illiquidity, and other factors affect long-term returns.

What Should You Do Instead?

If you arrived at this page because a company pitched you a home storage Gold IRA, the first step is to recognize the pitch for what it is: a prohibited structure wrapped in legal-sounding language. Here are three legitimate paths forward, depending on what you are actually trying to accomplish.

- Open a properly structured Gold IRA. If you want gold in your retirement portfolio with tax-deferred growth, work with a custodian that uses an IRS-approved depository. The metals stay in a vault, not in your home, but you retain ownership and can take physical delivery as a distribution at retirement age. Our Gold IRA resource center explains the full process.

- Buy physical gold outside your IRA. If what you really want is gold coins in your hand, use after-tax money. You lose the tax-deferred growth, but you gain complete control over storage, access, and timing. There are no custodian fees, no depository charges, and no risk of triggering a prohibited transaction.

- Consult a fee-only financial advisor or tax professional. A fee-only advisor has no incentive to sell you a particular product. They can model the tax impact of different approaches and help you decide whether a Gold IRA, personal gold ownership, or a combination makes sense for your situation. This is especially important for accounts above $100,000 where the stakes of a prohibited transaction are high.

When evaluating providers, confirm which custodians use approved depositories, what storage options they offer, and how their fee structures compare. Our provider comparison worksheet can help you track those details side by side.

One question worth asking: if home storage is clearly illegal, why do companies still sell it? The answer is economic. Home storage IRA setups generate $1,500 to $5,000 in LLC formation fees, plus ongoing annual charges, for a structure that costs the promoter very little to create. The investor bears all the tax risk. The promoter collects the fees regardless of what the IRS decides later (Source: Yahoo Finance).

We have also noticed that companies promoting home storage tend to be the same ones with unusually aggressive marketing tactics and high-pressure sales. The correlation is not coincidental. The LLC setup fee provides a large profit margin that funds heavy promotion. Our Gold IRA scams overview details how to identify these incentive structures before they cost you money (Source: LendEDU).

When to Talk to a Financial Advisor

Consider consulting a fee-only financial advisor before proceeding if any of these apply to your situation:

- A company told you home storage is legal and you want a second opinion

- You already have metals stored at home in an IRA structure

- You want to understand the tax consequences of correcting a prohibited transaction

Next step

Want to hold gold in a tax-advantaged account the right way? Learn how a Gold IRA works with proper custodian and depository setup, or review the fee breakdown to understand storage costs at IRS-compliant depositories.

Home storage Gold IRAs are not a gray area. The IRS code is explicit, the Tax Court has ruled, and the penalties are steep. The Taxable Moment — the instant you take personal possession of IRA metals — converts a tax-advantaged retirement account into a fully taxable distribution. No LLC structure, no home safe, and no clever paperwork changes that outcome.

If you want physical gold in your retirement plan, use a properly structured Gold IRA with an approved depository. If you want physical gold in your home, buy it with after-tax money. These are two separate goals with two separate solutions, and trying to combine them into one structure is what creates the tax liability. Understanding the distinction is the first step toward protecting both your metals and your retirement savings.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.