Gold IRA Risks

Gold IRA risks range from high fees to outright fraud, and marketing rarely mentions them. Fee-related complaints outnumber price-loss complaints in SEC and BBB filings by a wide margin, as documented in the SEC investor alert on self-directed IRAs. One wrong provider or overlooked rule can cost tens of thousands of dollars. This article ranks seven Gold IRA downsides from most common to most severe, with the numbers behind each.

Key Takeaways

- Fee problems, not price drops, cause the most Gold IRA complaints in regulatory filings and BBB records.

- Gold pays no dividends. Your return depends entirely on price gains, which must outpace fees first.

- The SEC shut down Red Rock Secured in 2023 over $76 million in losses. Fraud risk is real.

What Are the Main Risks of a Gold IRA?

A Gold IRA shares some risks with any retirement account, such as market fluctuations and tax penalties for early withdrawal. But it adds several risks that standard brokerage IRAs do not carry. Physical metals must be stored in an approved depository. Buying and selling involves dealer markups and buyback spreads that do not exist with stocks or ETFs. And the self-directed IRA structure gives custodians less oversight responsibility, which creates openings for dishonest dealers (Source: SEC Investor Alert on Self-Directed IRAs).

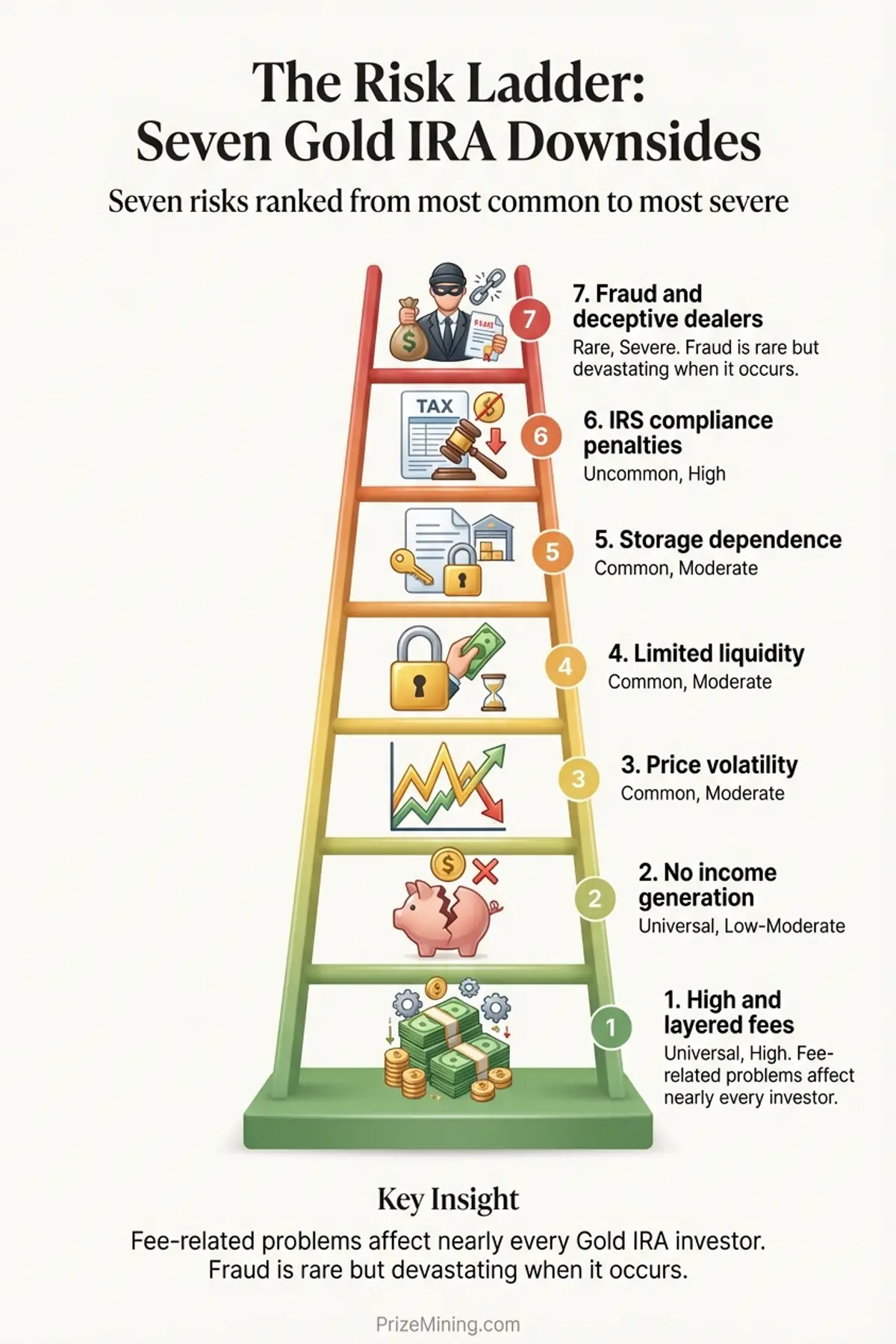

We organize these downsides into what we call “The Risk Ladder,” ranking seven risks from the most common to the most severe. The risks near the bottom of the ladder affect nearly every Gold IRA holder. The risks near the top affect fewer people, but the damage is far greater when they do.

What Are the Seven Downsides?

Think of these seven risks as rungs on a ladder. The bottom rungs are the ones nearly every Gold IRA investor steps on. The top rungs are rarer, but the fall is much harder. Understanding where each risk sits helps you focus your due diligence on the problems most likely to affect your money.

| Rank | Risk | How Common | Impact Level | Who It Affects Most |

|---|---|---|---|---|

| 1 | High and layered fees | Very common | Moderate | All investors, especially small accounts |

| 2 | No income generation | Inherent | Moderate | Retirees needing cash flow |

| 3 | Price volatility | Frequent | High | Short-term holders |

| 4 | Limited liquidity | Common | Moderate to high | Investors who need fast access |

| 5 | Storage dependence | Inherent | Low to moderate | All Gold IRA holders |

| 6 | IRS compliance risk | Uncommon | High | DIY investors, early withdrawers |

| 7 | Fraud and deceptive dealers | Rare | Severe | First-time precious metals buyers |

1. High and Layered Fees

Gold IRA fees work like a slow leak in a tire: each individual cost seems small, but together they drain value over time. You pay a setup fee to the custodian, an annual maintenance charge, a storage fee to the depository, a dealer markup when buying metals, and a buyback spread when selling. Five separate charges, often collected by three different companies.

On a $50,000 account, first-year costs typically range from $1,800 to $5,300, with the dealer markup accounting for the largest share. Annual ongoing costs run $250 to $600 per year after that. Over a decade, the cumulative fee drag can exceed 10% of your original investment. Our full breakdown of Gold IRA fees shows the math layer by layer (Source: Yahoo Finance).

2. No Income Generation

Stocks pay dividends. Bonds pay interest. Real estate investment trusts distribute rental income. Gold pays nothing. Holding gold in your IRA is like owning a painting — it may appreciate, but it never mails you a check. It sits in a vault and either goes up in price or goes down. Your entire return depends on selling the metal for more than you paid, after accounting for every fee along the way.

For investors who plan to live off their retirement accounts, this matters. A portfolio of dividend-paying stocks can produce 2% to 4% in annual income without selling a single share. A Gold IRA produces zero income regardless of its size. The only way to generate cash from a Gold IRA is to sell part of your holdings, which triggers the buyback spread and may create a taxable event (Source: IRS Publication 590-B).

3. Price Volatility

Gold is not as stable as many investors assume. In 2013, the price of gold dropped 28% in a single year. Between 2011 and 2015, gold lost roughly a third of its value before beginning a slow recovery. These are not ancient history; they are within the investment horizon of anyone approaching retirement today (Source: Yahoo Finance).

Gold's long-term trend has been upward, but that does not protect short-term holders. If you need to liquidate during a downturn, you sell at the depressed market price minus the buyback spread, a double hit. Volatility is most dangerous when it coincides with the point in your life when you actually need the money.

4. Limited Liquidity

Selling gold from an IRA is not like selling a stock. With stocks, you click a button and the proceeds settle in your brokerage account within one or two business days. With a Gold IRA, you must contact the custodian, instruct them to liquidate, wait for the dealer to provide a buyback quote, accept the quote, and then wait for funds to transfer. The process typically takes five to ten business days. In some cases it takes longer.

Liquidity in a Gold IRA is more like selling a house than selling stocks: it takes time, involves a spread, and you cannot do it instantly. If you need emergency access to retirement funds, a Gold IRA is one of the slowest vehicles to convert. Our Gold IRA liquidation overview covers the process step by step and explains how buyback programs work.

5. Storage Dependence

IRS rules require Gold IRA metals to be held in an approved depository. You cannot store them at home, in a safe deposit box, or in any location you personally control (Source: IRS Publication 590-A). That means you depend entirely on a third-party facility for the physical security and insurance of your retirement assets.

Most approved depositories are well-insured and highly secure. The risk is not that the vault gets robbed. The risk is that you have limited control over the facility, the insurance terms, and what happens if the depository changes ownership or policies. If you choose commingled storage, you receive equivalent metals when you withdraw, not necessarily the exact coins or bars you purchased. Segregated storage addresses that issue but costs more.

6. IRS Compliance Risk

Gold IRAs operate under the same IRS rules as other IRAs, with added complexity around eligible metals and storage requirements. If you buy metals that do not meet IRS fineness standards, store metals in an unapproved location, or take a distribution before age 59 and a half, the IRS may treat the transaction as a taxable distribution. The penalty is income tax on the full amount plus a 10% early withdrawal penalty (Source: IRS Publication 590-B).

Self-directed IRA custodians generally do not verify that your investment decisions comply with IRS rules. Their role is administrative, not advisory. IRS rules for Gold IRAs work like building codes — you may not notice them until an inspection reveals a violation. That places the compliance burden on you. Mistakes, even accidental ones, can result in significant tax bills. Understanding how a Gold IRA works at the structural level helps reduce this risk.

7. Fraud and Deceptive Dealers

The most severe risk on the ladder is fraud. In 2023, the SEC charged Red Rock Secured LLC and its principals with defrauding investors out of approximately $76 million. The company allegedly used high-pressure sales tactics, charged excessive undisclosed markups, and misrepresented the value and quality of metals sold to retirement investors.

Red Rock was not an isolated case. The precious metals industry has seen multiple enforcement actions involving dealers who overcharged for metals, sold non-IRA-eligible products, or simply took money and failed to deliver. Fraud does not affect most Gold IRA investors, but the consequences for those it does affect are devastating, often wiping out years of retirement savings. Our Gold IRA scams overview covers the warning signs in detail (Source: FTC Disclosure Guidelines).

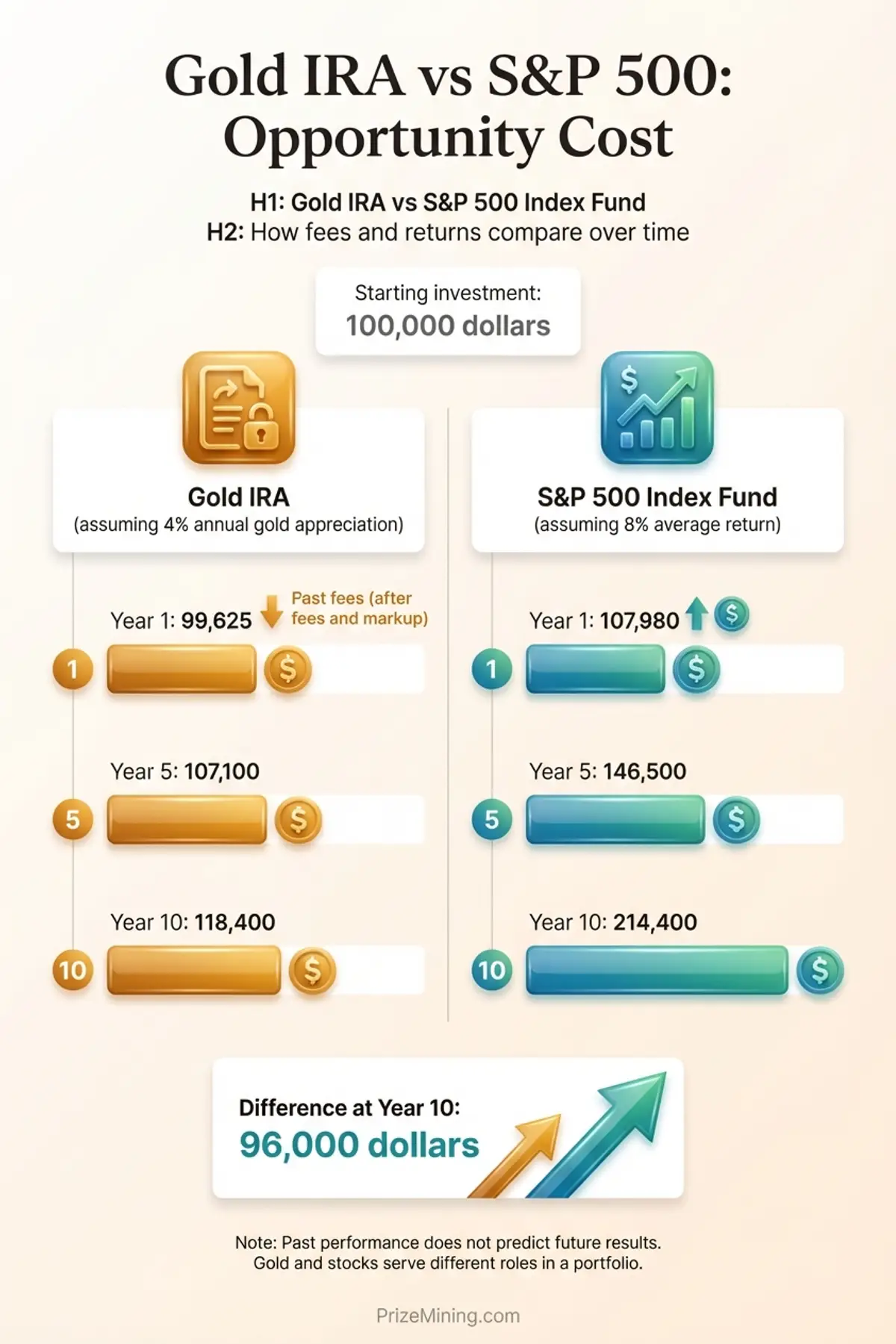

What Is the Opportunity Cost?

Every dollar in a Gold IRA is a dollar not invested somewhere else. That trade-off is the opportunity cost, and it may be the most overlooked risk of all. Over the ten-year period ending December 2024, the S&P 500 averaged roughly 12% per year while gold averaged roughly 8% per year (Source: Yahoo Finance). The table below shows what that gap looks like in dollar terms on a $100,000 investment, including the effect of Gold IRA fees.

| Investment | Year 1 | Year 5 | Year 10 |

|---|---|---|---|

| S&P 500 index fund (0.03% fee) | $111,970 | $176,200 | $310,600 |

| Gold IRA (8% return, fees included) | $101,620 | $140,300 | $196,700 |

| Difference | $10,350 | $35,900 | $113,900 |

Assumptions: S&P 500 at 12% annual return with a 0.03% expense ratio. Gold at 8% annual return with a 5% initial dealer markup, $375/year in custodian and storage fees, and a 3% buyback spread at liquidation. Past performance does not guarantee future results. Both scenarios use a $100,000 starting balance with no additional contributions.

After ten years, the S&P 500 investment is worth roughly $113,900 more than the Gold IRA. The gap comes from two places: the difference in annual returns and the fee drag that Gold IRAs carry. Even if gold matched the stock market's return rate, the Gold IRA would still trail because of its higher costs.

None of this means gold is a bad asset. Comparing a Gold IRA to an index fund is like comparing a savings account to a business — one preserves, the other compounds. Gold can serve as a portfolio diversifier and an inflation hedge. The point is that concentrating too much of your retirement in a Gold IRA has a measurable cost. Many financial planners suggest limiting precious metals to 5% to 10% of a retirement portfolio, not replacing the entire thing (Source: Investopedia).

Volatility Is Not the Same as Liquidity Risk

Investors often use “volatility” and “liquidity” interchangeably when discussing Gold IRA risks. They are two separate problems, and confusing them can lead to poor decisions.

Volatility refers to how much the price of gold moves up and down over time. A volatile asset changes in value quickly and unpredictably. Gold dropped 28% in 2013. It gained over 25% in 2020. Those swings are volatility. The risk is that your holdings lose value, but you still own them and can wait for a recovery.

Liquidity risk refers to how quickly and easily you can convert your holdings into cash without a significant loss beyond the market price. In a Gold IRA, liquidity risk comes from the multi-step selling process, the days-long settlement, and the buyback spread that reduces what you receive. Even when gold prices are stable, you face a cost and delay when selling.

The distinction matters because they require different responses. You manage volatility risk through allocation and time horizon. You manage liquidity risk by keeping enough liquid assets outside your Gold IRA to cover near-term needs. An investor who puts 80% of their retirement in a Gold IRA faces both problems at once: a price drop and an inability to sell quickly at a fair price.

What Red Flags Should You Watch For?

Not every Gold IRA provider is a scam. But the industry has enough bad actors that basic due diligence is essential. Opening a Gold IRA without research is like driving without a map: you may end up somewhere expensive. These five warning signs can help you filter out problematic companies before you send any money (Source: BBB).

- Pressure to act now. Any provider that insists you must commit today, claims a price is about to spike, or uses countdown timers and “limited-time” offers is using a high-pressure tactic. Reputable companies give you time to review materials and compare options.

- Promises of guaranteed returns. Gold prices are unpredictable. No dealer, custodian, or advisor can guarantee that gold will appreciate. Anyone who claims otherwise is misleading you. The SEC has cited guaranteed-return promises as a hallmark of precious metals fraud (Source: SEC Investor Alert on Self-Directed IRAs).

- No written fee schedule. If a provider will not give you a complete, written list of every fee, including the dealer markup on specific products, before you commit, treat that as a disqualifying red flag. Transparent companies publish their costs or provide them on request without hesitation.

- Unsolicited contact or celebrity endorsements. Cold calls, unsolicited emails, and celebrity-driven advertising do not indicate quality. Several companies facing SEC enforcement actions relied heavily on paid endorsements and outbound sales calls to acquire customers (Source: FTC Disclosure Guidelines).

- Unresolved complaints on the BBB or SEC actions. Before committing to any provider, check the Better Business Bureau for complaint history and the SEC's EDGAR database for enforcement actions. A pattern of unresolved complaints, especially about fees or delivery failures, suggests systemic problems.

When a Gold IRA May Not Be Right for You

A Gold IRA can fit into a well-built retirement plan. It can also be a poor choice depending on your circumstances. The situations below are not absolute rules, but they highlight conditions where the risks and costs tend to outweigh the potential benefits.

- Your total retirement savings are below $50,000. Fixed annual fees of $250 to $375 consume a disproportionate share of a small account. At $25,000, the fee drag alone exceeds 1% per year before gold needs to appreciate just to break even. A low-cost index fund IRA charges a fraction of those costs.

- You depend on your investments for regular income. Gold generates no dividends, interest, or distributions. If your retirement budget requires periodic cash flow, dividend stocks, bonds, or annuities may serve that need at a lower cost and with greater predictability.

- Your time horizon is under five years. The round-trip cost of buying and selling metals, including dealer markup and buyback spread, can reach 8% to 15%. Short holding periods rarely allow enough price appreciation to overcome that entry-and-exit cost.

- You are not willing to research providers carefully. Unlike a standard IRA at a major brokerage, where fees are standardized and regulation is tight, Gold IRAs require you to evaluate multiple parties: the custodian, the dealer, and the depository. Investors who skip this step are more likely to overpay or encounter deceptive practices.

- You plan to allocate more than 10% to 15% of your retirement to precious metals. Most fee-only financial advisors suggest limiting alternative assets like gold to a single-digit percentage of your total portfolio. Overconcentration amplifies every risk on the ladder, from fees to volatility to liquidity.

Talk to a fee-only financial advisor before committing. An independent advisor who does not earn commissions on Gold IRA sales can evaluate whether precious metals belong in your specific plan and, if so, at what allocation (Source: Investopedia).

How Can You Reduce These Risks?

You cannot eliminate Gold IRA risks entirely, but you can manage them. The following steps address the most common and most damaging problems investors encounter.

Compare at least three providers

Request a complete written fee schedule from each, including the dealer markup on specific products. Side-by-side comparison is the single most effective way to avoid overpaying. You can use our provider comparison worksheet to start that process.

Keep your allocation modest

Limiting gold to 5% to 10% of your overall retirement portfolio reduces the impact of every risk on the ladder. If gold drops 28% in a single year and represents 5% of your portfolio, your total loss from that position is 1.4%. If gold represents 50% of your portfolio, that same drop costs 14%.

Verify the provider before sending money

Check the SEC's EDGAR database, FINRA BrokerCheck, and the Better Business Bureau. Look for enforcement actions, unresolved complaints, and licensing status. Five minutes of verification can prevent catastrophic losses (Source: BBB).

Understand the IRS rules before buying

Know which metals qualify, where they must be stored, and what triggers a taxable distribution. The IRS does not give partial credit for honest mistakes. Read how a Gold IRA works to understand the structural requirements (Source: IRS Publication 590-A).

Maintain liquid reserves outside your Gold IRA

Because selling metals from an IRA takes days and involves a spread, keep enough liquid assets in other accounts to cover six months or more of expenses. This prevents you from being forced to liquidate gold during a downturn or on an unfavorable timeline.

What Should You Research Next?

Understanding risks is the first step. The next step is understanding the specific mechanics and costs that drive those risks. Each of the resources below digs deeper into one aspect of Gold IRA ownership.

- Gold IRA fees explained — a layer-by-layer breakdown of what you will actually pay, with cost examples for $50K and $100K accounts.

- Gold IRA scams — case studies of fraud, pressure tactics, and the red flags that precede them.

- Gold IRA liquidation — how the selling process works, what buyback spreads to expect, and how to plan a distribution.

- How a Gold IRA works — the structural basics, from custodians and depositories to eligible metals and IRS rules.

- Gold IRA fees breakdown — how custodian charges, storage costs, and dealer markups affect your returns.

- Our review methodology — how we evaluate providers, including the criteria for fee transparency, complaint history, and regulatory standing.

Next step

Risks are easier to manage when you know the costs. Read the full fees breakdown to see exactly what you will pay, or return to the Gold IRA resource center for a full breakdown.

Gold IRAs carry real risks that go beyond price fluctuations. The Risk Ladder puts those downsides in order: fees are the most common problem, fraud is the most damaging, and several other risks sit between. None of these downsides make a Gold IRA inherently bad, but all of them make due diligence essential.

The investors who fare best with Gold IRAs tend to share a few traits: they keep their allocation modest, they compare multiple providers before committing, they understand the fee structure, and they consult an independent advisor. The investors who fare worst tend to rush in without research, concentrate too much of their retirement in one asset, or respond to high-pressure sales tactics. The difference between those two outcomes comes down to preparation.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.