Gold IRA Tax Rules

Gold IRA taxes confuse investors because the rules feel unfamiliar. The IRS taxes precious metals IRAs the same as any other retirement account, as detailed in IRS Publication 590-A. A single mistake with contributions, withdrawals, or prohibited transactions can cost thousands. This article covers every tax phase, from funding to distribution, plus the penalties to avoid.

Consult a tax professional before making Gold IRA decisions. This article is educational and does not constitute tax advice.

Key Takeaways

- Gold IRAs follow standard IRA tax rules: Traditional accounts defer taxes until withdrawal, Roth accounts pay taxes upfront and withdraw tax-free.

- Withdrawing before age 59½ triggers a 10% penalty plus income tax, and missing a required minimum distribution carries a 25% penalty.

- Prohibited transactions like home storage or buying from family members can disqualify your entire IRA, making the full balance taxable immediately.

How Are Gold IRAs Taxed?

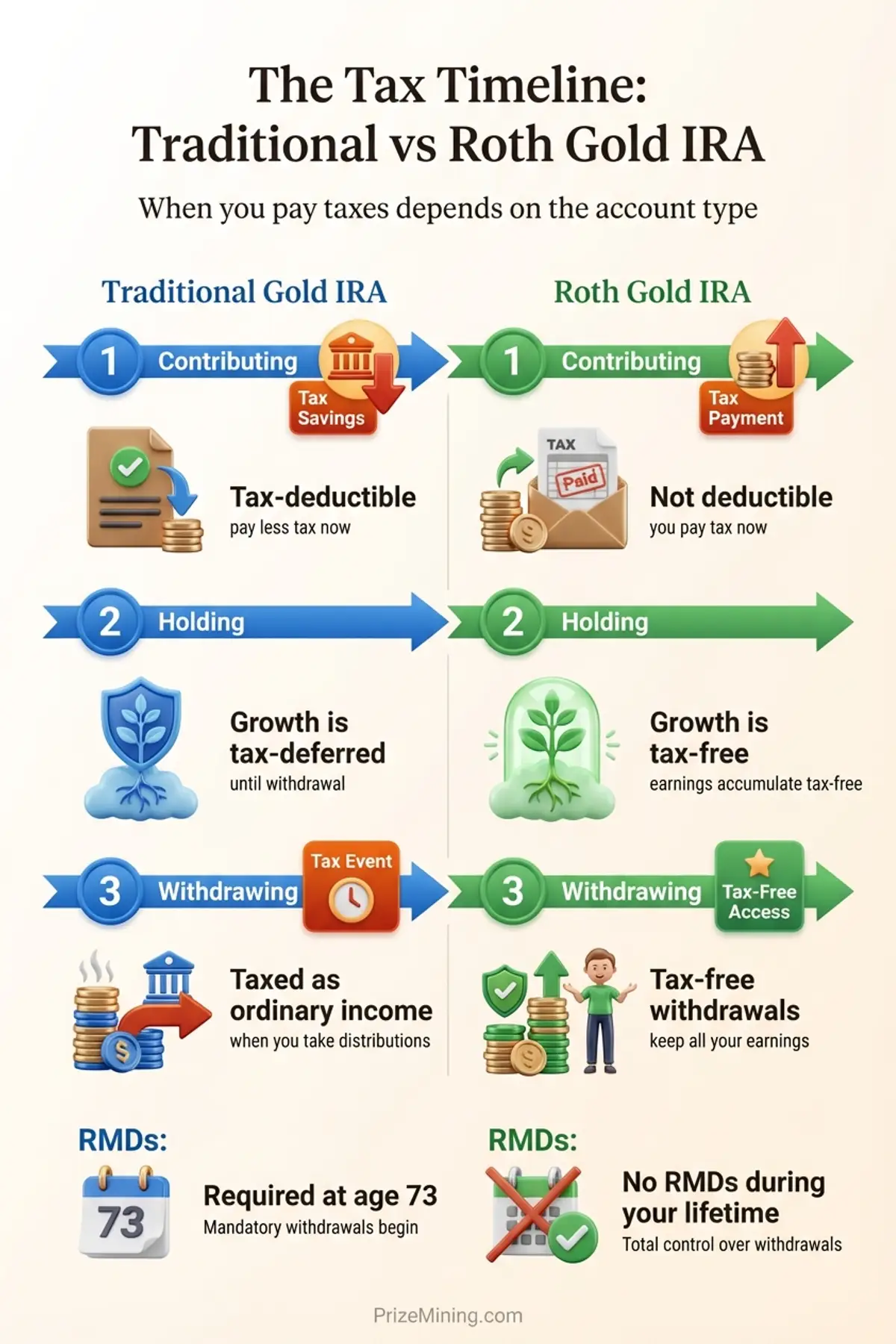

Gold IRAs are taxed in three phases: when you put money in, while it grows, and when you take money out. The tax treatment at each phase depends on whether you hold a Traditional or Roth account. Understanding those three phases, what we call “The Tax Timeline,” is the foundation for every decision that follows.

Think of a Traditional Gold IRA like a tax bill you defer. The government lets you invest pretax money now, but collects the full bill when you withdraw. A Roth Gold IRA works the opposite way: you pay the restaurant bill before the meal. You contribute after-tax dollars today, then withdraw, including all growth, without owing anything more (Source: IRS Publication 590-A).

Both account types hold the same metals and follow the same custody and storage rules. The difference is entirely about timing: when does the IRS collect its share? If you are not yet familiar with how Gold IRAs work, that guide covers the structural basics before you dive into tax specifics.

How Does the Tax Timeline Work?

Every dollar in your Gold IRA passes through three tax phases. The table below shows how Traditional and Roth accounts handle each phase differently (Source: IRS Publication 590-A, IRS Publication 590-B).

| Phase | Traditional Gold IRA | Roth Gold IRA |

|---|---|---|

| Phase 1 — Contributing | Contributions may be tax-deductible (income limits apply) | Contributions are made with after-tax dollars (no deduction) |

| Phase 2 — Holding and Growth | Growth is tax-deferred (no annual tax on gains) | Growth is tax-free (no tax on gains, ever) |

| Phase 3 — Withdrawing | Withdrawals taxed as ordinary income | Qualified withdrawals are completely tax-free |

Phase 1 — Contributing

For 2024 and 2025, the IRS sets the annual IRA contribution limit at $7,000 for individuals under age 50 and $8,000 for those 50 and older. This limit applies across all your IRAs combined, not per account (Source: IRS Publication 590-A).

| Age | Annual Limit | Catch-Up Amount |

|---|---|---|

| Under 50 | $7,000 | — |

| 50 and older | $8,000 | $1,000 |

Contribution limits work like a speed limit — the number is the same for everyone, but the penalty for going over depends on how fast you were going. With a Traditional Gold IRA, your contribution may be tax-deductible if you meet income requirements. If you or your spouse participates in a workplace retirement plan, the deduction phases out at certain modified adjusted gross income (MAGI) levels. Contributing more than the annual limit triggers a 6% excise tax on the excess amount for every year it remains in the account (Source: 26 U.S. Code § 408).

Roth Gold IRAs have their own income limits for eligibility. High earners may not be able to contribute directly. The contribution itself is never deductible, which is the tradeoff for tax-free withdrawals later.

Phase 2 — Holding and Growth

While your gold sits in the IRA, you owe no annual tax on price appreciation. In a Traditional account, this is called tax-deferred growth: you will pay income tax on the gains when you eventually withdraw. In a Roth account, growth is tax-free entirely, provided you meet the five-year holding rule and are at least 59½ at withdrawal.

This holding-phase advantage is the primary reason retirement accounts exist. Outside an IRA, selling gold at a profit triggers capital gains tax in the year of the sale. Physical gold held outside an IRA is classified as a collectible and taxed at up to 28%, higher than the 20% maximum long-term capital gains rate that applies to stocks (Source: IRS Publication 590-B).

Phase 3 — Withdrawing and Distributing

In a Traditional Gold IRA, every dollar you withdraw is taxed as ordinary income at your current marginal rate. If you are in the 24% bracket and withdraw $50,000, you owe $12,000 in federal income tax on that distribution. The IRS does not distinguish between your original contributions and the growth. It all gets taxed on the way out.

In a Roth Gold IRA, qualified withdrawals are tax-free. You already paid tax on the money before it went in. Both contributions and growth come out without additional tax, assuming the account has been open for at least five years and you are 59½ or older.

Traditional vs Roth Gold IRA — Which Pays Less Tax?

Investors frequently confuse Traditional and Roth Gold IRAs, assuming one is universally better. The answer depends on your current tax bracket, your expected bracket in retirement, and how long you plan to hold the account. The comparison table below puts the key differences side by side (Source: IRS Publication 590-A, IRS Publication 590-B).

| Feature | Traditional Gold IRA | Roth Gold IRA |

|---|---|---|

| Tax deduction | Contributions may be deductible | No deduction |

| Growth | Tax-deferred | Tax-free |

| Withdrawal tax | Taxed as ordinary income | Tax-free (if qualified) |

| RMDs required | Yes, starting at age 73 | No, not during owner's lifetime |

| Income limits | Deduction limited by income if covered by employer plan | Direct contributions phased out at higher incomes |

| Best suited for | Investors expecting a lower tax bracket in retirement | Investors expecting the same or higher bracket in retirement |

When we first compared Traditional and Roth Gold IRAs, we focused on the upfront tax deduction. After modeling five and ten-year scenarios, the Roth advantage at distribution, particularly avoiding forced RMD sales at unfavorable prices, proved more valuable for most investors with long time horizons. That said, the Traditional deduction provides immediate tax savings that benefit investors in high brackets today who expect lower income in retirement.

Neither account type is universally better. A tax professional can model your specific situation. If you are rolling over an existing 401(k) or IRA, the rollover type (direct vs. indirect) also affects your tax treatment.

What Happens If You Withdraw Early?

Taking money out of a Gold IRA before age 59½ typically triggers two costs: ordinary income tax on the distribution amount (for Traditional accounts) and a 10% early withdrawal penalty on top of that. Withdrawing early from a Traditional Gold IRA is like breaking a lease — you pay the remaining obligation plus a penalty fee. The combination can consume a third or more of the withdrawn amount (Source: IRS Publication 590-B).

Here is what an early withdrawal looks like in practice for a Traditional Gold IRA.

| Component | Amount |

|---|---|

| Early withdrawal amount | $50,000 |

| Federal income tax (24% bracket) | $12,000 |

| 10% early withdrawal penalty | $5,000 |

| Total tax cost | $17,000 |

| Net amount received | $33,000 |

In this example, $17,000 of a $50,000 withdrawal goes to taxes and penalties. That is 34% of the distribution. State income taxes, if applicable, would reduce the net amount further.

Certain exceptions can waive the 10% penalty, though income tax still applies. These include disability, certain medical expenses exceeding 7.5% of adjusted gross income, and substantially equal periodic payments under IRS Rule 72(t). The exceptions are narrow, and qualifying requires careful documentation. For a broader view of the financial risks involved, our Gold IRA risks guide covers penalty exposure alongside other concerns (Source: IRS Publication 590-B).

How Do RMDs Work for Gold IRAs?

Required minimum distributions are like a mandatory rent payment: whether gold prices are up or down, you owe the withdrawal. Traditional Gold IRA holders must begin taking RMDs at age 73 under current IRS rules. Roth Gold IRAs have no RMDs during the owner's lifetime, which is one of their most significant structural advantages (Source: IRS RMD FAQs).

The IRS calculates your RMD by dividing your account balance as of December 31 of the prior year by a life expectancy factor from the Uniform Lifetime Table. For example, at age 75, the divisor is approximately 24.6. On a $200,000 Traditional Gold IRA, the RMD would be roughly $8,130 that year.

Missing an RMD carries a 25% penalty on the amount you should have withdrawn. If you correct the shortfall within two years, the penalty drops to 10%. Either way, it is one of the steepest penalties in the IRA tax code (Source: IRS Publication 590-B). Our RMD rules overview covers the full calculation method, the Uniform Lifetime Table, and strategies for avoiding the penalty.

The RMD Liquidity Problem

Here is where Gold IRAs create a practical challenge that paper-asset IRAs do not. When your Traditional IRA holds stocks or mutual funds, meeting an RMD is straightforward: your custodian sells shares at market price and sends the cash. The transaction settles in one or two business days with minimal spread.

With a Gold IRA, the process is more involved. Your custodian must coordinate with the depository to liquidate physical metals. The dealer who buys back your gold typically offers 1% to 5% below the spot price, the same buyback spread described in our Gold IRA fees breakdown. The transaction can take days or weeks to settle, and you do not control exactly when the sale executes.

That timing gap matters. If gold drops between when you request the sale and when it executes, you receive less. If gold rises after you sell, you have lost that upside. And you absorb the buyback spread regardless of price direction. On an $8,130 RMD with a 3% buyback spread, you lose roughly $244 just to convert the gold to cash, before any tax is calculated.

Roth Gold IRAs avoid this problem entirely during the owner's lifetime because no RMDs are required. You sell metals only when you choose to, at a time that works for you.

What Prohibited Transactions Trigger Penalties?

The IRS defines prohibited transactions as certain dealings between your IRA and “disqualified persons,” which include you, your spouse, your lineal descendants, and entities you control. Self-dealing with your IRA is like a referee betting on the game — the rules exist specifically to prevent it. Violating these rules does not result in a small fine. It can cause the IRS to treat your entire IRA as distributed, making the full account balance taxable in a single year, plus the 10% early withdrawal penalty if you are under 59½ (see the IRS prohibited transactions rules).

Four prohibited transaction traps catch Gold IRA investors more often than others.

- Home storage of IRA metals. Keeping your IRA gold at home, in a personal safe, or in a safe deposit box you control is a prohibited transaction. The IRS requires IRA metals to be held by an approved custodian at a qualified depository. Companies that promote “home storage Gold IRAs” are promoting a structure the IRS has repeatedly challenged. Our home storage Gold IRA guide covers the legal risks in detail (Source: SEC Investor Alert on Self-Directed IRAs).

- Buying metals from a family member. Purchasing gold coins from your spouse, parent, child, or grandchild and placing them in your IRA is a prohibited transaction. The IRS treats this as self-dealing even if the price is fair market value. All IRA purchases must go through an arms-length dealer.

- Using IRA metals for personal purposes. Wearing jewelry purchased by your IRA, displaying IRA-owned coins in your home, or using IRA gold as collateral for a personal loan all constitute prohibited use. The metals belong to the IRA, not to you personally, until they are formally distributed.

- Self-dealing through a controlled entity. If you own a business and that business sells gold to your IRA, or if your IRA lends money to a business you own, the transaction is prohibited. The IRS draws the line broadly. Any transaction that benefits you or a disqualified person, directly or indirectly, falls outside allowed activity (Source: IRS Prohibited Transactions).

The consequence of any single prohibited transaction can be severe. If the IRS determines your IRA engaged in a prohibited transaction, the account may be treated as fully distributed on the first day of the year in which the violation occurred. On a $100,000 Traditional IRA for someone under 59½ in the 24% bracket, that could mean $24,000 in income tax plus $10,000 in early withdrawal penalties, a $34,000 cost for a single rule violation.

What Tax Mistakes Cost Investors Money?

Tax penalties in Gold IRAs rarely come from deliberate evasion. They come from misunderstanding the rules or assuming gold is treated differently from other IRA assets. These four mistakes appear repeatedly.

- Contributing more than the annual limit. The $7,000 limit (or $8,000 for those 50 and older) applies across all your IRAs combined. If you contribute $5,000 to a Traditional IRA and $4,000 to a Gold IRA in the same year, you have exceeded the limit by $2,000. The IRS charges a 6% excise tax on excess contributions for every year the excess remains in the account. Correct it by withdrawing the excess before your tax filing deadline (Source: IRS Publication 590-A).

- Missing the 60-day indirect rollover window. If you receive funds from a previous retirement account and intend to roll them into a Gold IRA, you have 60 days to complete the deposit. Missing the deadline means the entire amount is treated as a taxable distribution. A direct rollover avoids this risk entirely because the funds transfer between custodians without you touching them (Source: IRS Rollovers page).

- Forgetting state taxes on distributions. Federal income tax is only part of the cost. Most states tax IRA distributions as ordinary income. Depending on your state, the combined federal and state rate on a Traditional Gold IRA withdrawal can exceed 30%. Factor state taxes into your distribution planning.

- Assuming gold gains receive capital gains treatment inside an IRA. Outside a retirement account, gold is taxed as a collectible at up to 28%. Inside a Traditional IRA, withdrawals are taxed as ordinary income, which can be higher or lower than 28% depending on your bracket. Do not assume the IRA wrapper automatically reduces your tax rate on gold, it changes the timing and the type of tax, not always the amount (Source: CBS News).

When the Tax Math May Not Work in Your Favor

The tax advantages of a Gold IRA are real, but they do not benefit every investor equally. Before committing, consider whether any of these situations apply to you.

- You expect to be in a higher tax bracket now than in retirement. If your current income is high and you anticipate lower income after you stop working, a Traditional IRA deduction saves you more today than a Roth conversion costs. Converting to Roth while you are in a peak earning year means paying tax at your highest rate, which defeats the purpose of the conversion for many investors.

- Your account is too small for the fixed fees to be offset by tax benefits. Gold IRA custodians charge flat annual fees regardless of account size. On a small balance, those fees consume a larger percentage of your assets each year, and the tax deferral or tax-free growth may not generate enough savings to overcome the drag. Run the numbers before assuming the tax wrapper pays for itself.

- You plan to withdraw within five years. Short holding periods leave little time for tax-deferred or tax-free growth to compound. When you add early withdrawal penalties, income taxes, and the buyback spread on physical metals, the total cost of a round trip in under five years can erase the tax benefit entirely.

- You already have significant tax-deferred assets and adding more creates a large RMD burden at 73. Every dollar in a Traditional IRA increases your required minimum distribution. If you already hold substantial tax-deferred balances across multiple accounts, adding another Traditional Gold IRA makes the RMD math worse. Larger forced distributions can push you into a higher bracket, increase Medicare premiums, and trigger taxation of Social Security benefits.

Talk to a fee-only financial advisor or tax professional before opening a Gold IRA. An independent review of your tax situation, account balances, and retirement timeline can reveal whether the tax math works in your favor or against it.

What Should You Ask Your Tax Advisor?

Gold IRA tax rules interact with your broader financial picture in ways that generic articles cannot fully address. Before opening or funding a precious metals IRA, a conversation with a qualified tax professional can prevent costly mistakes. Here are five specific questions worth asking.

- Am I eligible for a tax deduction on Traditional IRA contributions? Your eligibility depends on your income, filing status, and whether you or your spouse participates in a workplace retirement plan. The answer determines whether a Traditional Gold IRA offers any upfront tax benefit for your situation.

- Should I choose Traditional or Roth based on my current and projected tax bracket? If you expect your income to drop in retirement, Traditional may save more. If you expect your bracket to stay the same or rise, Roth may cost less over the life of the account.

- How will RMDs from a Gold IRA affect my other retirement income? RMDs from a Traditional Gold IRA add to your taxable income, which can push you into a higher bracket, increase Medicare premiums, and trigger taxation of Social Security benefits.

- What are the tax consequences of my planned rollover? Rolling over a Traditional 401(k) into a Roth Gold IRA triggers a taxable conversion. Rolling into a Traditional Gold IRA does not, if done as a direct transfer. Your advisor can model the tax impact of each path.

- Does my estate plan account for inherited IRA rules? Beneficiaries who inherit a Traditional Gold IRA generally must withdraw the entire balance within ten years, creating potential tax burdens. A Roth Gold IRA passes to heirs tax-free, though the ten-year withdrawal window still applies for most non-spouse beneficiaries.

For a complete overview of Gold IRA structures, costs, and provider options, return to our Gold IRA resource center.

Next step

Understand the costs before you commit. Read our Gold IRA fees breakdown to see how custodian charges, storage costs, and dealer markups affect your account alongside taxes.

Gold IRA tax rules are not about gold. They are about the IRA wrapper surrounding it. The Tax Timeline, from contribution to holding to distribution, determines when and how much you owe. Traditional accounts defer the bill. Roth accounts settle it upfront. Prohibited transactions can shred the entire structure in a single violation.

Every figure in this article comes from IRS publications and federal statute, but tax law applies to individual circumstances in ways that general guidance cannot capture. Work with a qualified tax professional who understands self-directed retirement accounts. The cost of one planning session is small compared to the penalties for getting these rules wrong.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.