Spot Price vs Premium

You look up the gold price and see $2,300 per ounce, but a dealer quotes you $2,415. According to the Gainesville Coins Premiums Tracker, retail gold premiums ranged from 2% to over 10% above spot in 2024 and 2025, depending on the product. That spread means the difference between a fair deal and an overpriced one can cost you hundreds of dollars on a single purchase. This page breaks down what the premium covers, what typical ranges look like across bars and coins, and how to spot pricing that does not add up (Source: Gainesville Coins Premiums Tracker).

Key Takeaways

- Spot price is the wholesale exchange price. Retail price is spot plus premium. You always pay the retail price.

- Premiums cover real costs: refining, minting, distribution, insurance, and dealer margin.

- Gold bars typically carry 2% to 5% premiums; coins run 4% to 10%. Silver premiums are proportionally higher.

What Is the Spot Price?

The spot price is the current price for one troy ounce of a metal on major commodity exchanges. For gold, the two most referenced benchmarks are the LBMA Gold Price (set twice daily in London) and the COMEX futures price (traded on the CME Group in New York). These prices reflect wholesale transactions between banks, refiners, central banks, and large institutional traders (Source: LBMA Precious Metal Prices).

Think of the spot price like the wholesale price a grocery chain pays for oranges at a distribution center. That price is real, but you will never see it on the shelf at your local store. The store has to pay for transportation, refrigeration, labor, rent, and margin before it can sell you a single orange. The spot price of gold works the same way: it is the starting point, not the final price.

A common point of confusion is the difference between “spot price” and “retail price.” Many first-time buyers see the spot price on a financial website and assume that is what they will pay at a dealer. It is not. The spot price is the exchange-level wholesale price for large, unfinished bars traded between institutions. The retail price, which includes the premium, is what individual buyers pay for a finished product they can hold in their hand or store in a depository. Confusing the two leads to unrealistic expectations and sometimes to falling for dealers who imply they sell “at spot.”

What Is a Premium — and What Does It Cover?

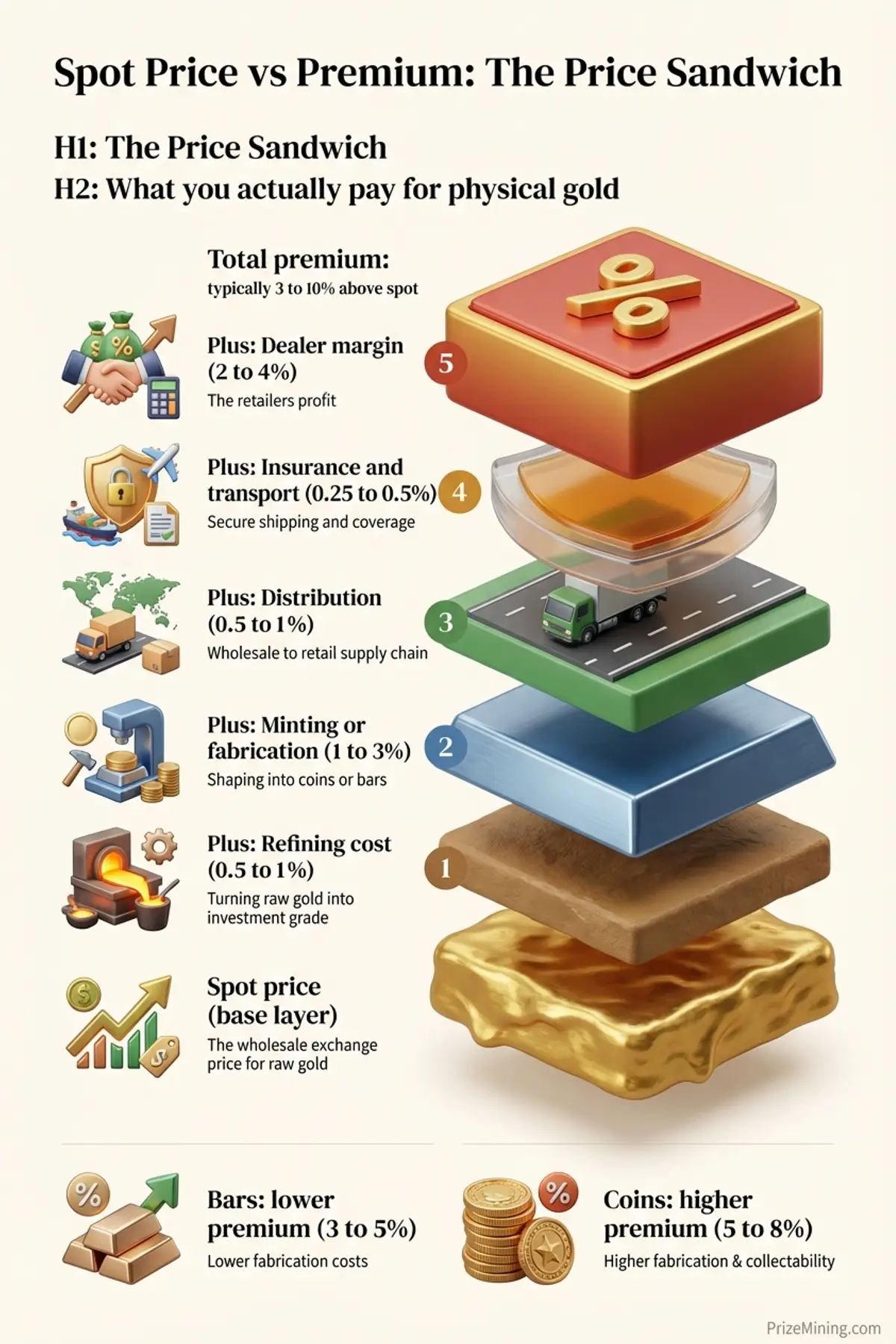

The premium is the amount added on top of the spot price to arrive at the retail price. We call this structure “The Price Sandwich.” The spot price is the base layer, the bread on the bottom. Stacked on top of it are the costs of turning a raw commodity into a finished, deliverable product: refining, minting, distribution, insurance, and dealer margin. Each layer adds cost, and together they form the retail price you actually pay.

The Price Sandwich is useful because it shows that premiums are not arbitrary markups. Each layer exists for a reason, and each one is paid to a different party in the supply chain. Here is what each layer covers.

| Premium Layer | What It Covers | Typical Share | Who Receives It |

|---|---|---|---|

| Refining | Purifying raw gold to 99.5% or 99.99% fineness | 0.5% – 1.0% | Refiner (PAMP, Valcambi, etc.) |

| Minting | Striking bars or coins with design, weight, assay | 0.5% – 3.0% | Mint (US Mint, Royal Canadian Mint, etc.) |

| Distribution | Shipping, armored transport, wholesale logistics | 0.3% – 0.8% | Distributor / wholesaler |

| Insurance | Transit and inventory coverage against loss or theft | 0.1% – 0.3% | Insurance underwriter |

| Dealer margin | Retail overhead, staff, website, compliance, profit | 1.0% – 5.0% | Retail dealer |

Another way to picture it: the premium is like the fare on a rideshare app. The base fare (spot price) is what the ride theoretically costs in fuel. But you also pay for the driver’s time, the platform’s cut, insurance, and a booking fee. The total is always more than the fuel cost, and that is not a scam — it is the cost of getting the service delivered to you.

For a deeper look at how dealer markups fit into the broader cost picture of a Gold IRA, see our Gold IRA fees breakdown. The premium is just one of several fee layers that affect your total cost.

How Do Premiums Differ Between Bars and Coins?

Premiums vary widely depending on the product type, the metal, the size, and the dealer. Bars generally carry lower premiums than coins because they are cheaper to produce. Government-issued coins carry higher premiums because of minting costs, legal tender status, and collector demand. Smaller products carry higher percentage premiums because the fixed costs of manufacturing represent a larger share of the product value (Source: Gainesville Coins Premiums Tracker).

| Product | Type | Typical Premium | Notes |

|---|---|---|---|

| Gold 1 oz bar | Bar | 2% – 5% | Lowest premium for gold; IRA-eligible if .995+ |

| Gold American Eagle (1 oz) | Coin | 4% – 8% | Most popular IRA coin; higher mint cost |

| Gold Canadian Maple Leaf (1 oz) | Coin | 3% – 6% | 99.99% purity; slightly lower premium than Eagle |

| Silver 1 oz bar | Bar | 5% – 12% | Higher percentage due to lower base price |

| Silver American Eagle (1 oz) | Coin | 8% – 20% | Fixed mint cost is large relative to ~$30 spot |

| Platinum 1 oz bar | Bar | 3% – 7% | Thinner market; premiums more volatile |

| Palladium 1 oz bar | Bar | 5% – 10% | Limited retail supply; highest bar premium |

Silver premiums deserve special attention. Because silver trades around $28 to $32 per ounce while gold trades above $2,000, the fixed costs of minting and shipping a single coin take up a much larger percentage of the total price. A $3 premium on a $30 silver coin is 10%, while a $90 premium on a $2,300 gold coin is under 4%. This is not a dealer trick — it is math. If you are buying metals for an IRA, our IRA-eligible metals overview explains how purity requirements further narrow your options and can affect premiums.

Why Do Premiums Change?

Premiums are not static. They move based on supply and demand in the physical market, which is a different market from the paper futures market that sets the spot price. When demand for physical products surges faster than mints and refiners can produce, premiums expand. When demand cools and dealer inventories are full, premiums compress.

The clearest example in recent memory came in early 2020, when COVID-19 disrupted refinery operations while retail demand spiked. Premiums on American Gold Eagles jumped from around 5% to over 10% in a matter of weeks. Silver Eagles saw premiums exceed 50% above spot in some cases. The spot price and the retail price temporarily disconnected in a way that shocked even experienced buyers (Source: COMEX Gold Futures data).

The lesson I took from watching dealer premiums during the 2020 and 2022 supply crunches is that the worst time to buy physical metals is the moment everyone else wants to buy them too. Premiums spike precisely when fear is highest, which means panic buyers pay the most and patient buyers pay the least. It works like surge pricing on a rideshare app during a rainstorm: the underlying cost of the ride has not changed, but the sudden flood of demand lets the platform charge more because everyone wants a car at the same time.

Several factors drive premium fluctuations:

- Retail demand surges. Economic uncertainty, inflation fears, or geopolitical crises send retail buyers rushing to dealers, driving up premiums.

- Mint production limits. Government mints have finite capacity. When the US Mint rations Silver Eagle production, premiums soar on existing inventory.

- Supply chain disruptions. Refinery shutdowns, shipping delays, and raw material shortages tighten physical supply.

- Currency movements. A weaker dollar can increase domestic demand while making imports more expensive, pushing premiums higher.

- Dealer inventory levels. When dealers are flush with inventory, competition pushes premiums down. When shelves are bare, dealers charge more.

How to Compare Dealer Pricing

After spending two years comparing premiums across dealers for our research, the single most useful habit I developed was converting every quoted price to a percentage above spot before comparing anything. Dollar amounts are misleading when spot prices change daily. Percentages give you a stable basis for comparison.

Here is a simple process that works:

- Check the current spot price on a neutral source like Kitco, LBMA, or COMEX. Do not use the dealer’s own spot price display — some dealers show a slightly adjusted figure.

- Get the dealer’s price for a specific product — for example, a 1 oz Gold American Eagle. Make sure you are comparing the same product across dealers.

- Calculate the premium. Subtract spot from the dealer’s price, then divide by spot. If spot is $2,300 and the dealer charges $2,438, the premium is ($2,438 − $2,300) / $2,300 = 6.0%.

- Repeat with at least three dealers on the same day, at roughly the same time, since spot fluctuates throughout the trading session.

- Factor in shipping and insurance. Some dealers offer “free shipping” but bake the cost into a higher premium. Compare the all-in delivered price.

Think of comparing dealer premiums like comparing airline tickets. The base fare (spot price) is the same route for everyone. What varies is the fees, surcharges, and extras each airline adds on top. You would never compare a “base fare” from one airline to the “total price” from another. The same discipline applies to gold pricing.

Understanding how the Gold IRA process works can also help you evaluate whether a dealer’s premium includes IRA-specific services like custodian coordination and depository shipping, which are legitimate added costs.

What Pricing Red Flags Should You Watch For?

Most dealers charge fair premiums. But some use pricing structures designed to obscure how much you are actually paying. Knowing the warning signs protects you from overpaying by hundreds or thousands of dollars.

- “At spot” or “below spot” claims. No dealer sells finished products at or below the spot price. The costs of refining, minting, and distribution make it impossible. If a dealer advertises products “at spot,” they are either using a loss leader to get you into higher-margin products, or the claim is simply false. Our Gold IRA scams overview covers this tactic in detail.

- No live pricing on the website. Reputable dealers display real-time or near-real-time prices tied to the spot market. If a dealer requires you to call for a price, they may be quoting different premiums to different customers based on how informed they seem.

- Premiums above 10% on standard 1 oz gold bars. During normal market conditions, a 1 oz gold bar from a major refiner should carry a premium of 2% to 5%. If you are being quoted 10% or more outside of a genuine supply crisis, you are overpaying (Source: US Gold Bureau pricing reference).

- Pushing “exclusive” or “rare” coins. Some dealers steer customers away from standard bullion toward high-premium “collectible” or “proof” coins that carry markups of 30% to 50% or more. These products are harder to resell at fair value and are often not IRA-eligible.

- Bundling the premium into a “package deal.” If a dealer offers a diversified metals package without breaking out the per-product cost, you cannot verify whether each item is fairly priced. Always ask for itemized pricing.

The simplest protection is comparing three or more dealers on the same product, on the same day. If one dealer’s price is dramatically different from the others, that difference needs an explanation.

When to Talk to a Financial Advisor

Consider consulting a fee-only financial advisor before proceeding if any of these apply to your situation:

- You are quoted a premium that seems significantly above market norms

- You want an independent assessment of whether dealer pricing is fair

- You are comparing premiums across dealers and need help interpreting the differences

Where Premiums Fit in the Bigger Picture

The premium you pay at purchase is the first cost layer, but it is not the last. If you are buying metals for a Gold IRA, the premium sits alongside custodian fees, storage fees, and eventually a buyback spread when you sell. Our complete fee breakdown shows how all five layers stack up, and why comparing premiums in isolation can be misleading.

For buyers who are still exploring whether precious metals belong in their retirement strategy, the precious metals resource center covers the fundamentals: which metals exist, how they are traded, and what roles they can play in a portfolio. And if you are specifically considering a tax-advantaged account, the Gold IRA hub connects everything from provider reviews to rollover mechanics.

Understanding the Price Sandwich, the layers between the spot price and the price you pay, is one of the most practical edges an investor can have. It will not eliminate the premium, but it will help you recognize a fair one, avoid an inflated one, and make purchasing decisions with confidence rather than confusion.

Next step

Ready to see what qualifies for a tax-advantaged account? Check the IRA-eligible metals list to find out which products meet purity requirements, or review the full Gold IRA fee stack to see how premiums fit into your total cost.

The spot price is where every gold transaction begins, but no buyer’s process ends there. The premium is the cost of turning a commodity quote on a screen into a finished product in your hand or your depository. It covers refining, minting, distribution, insurance, and dealer margin — the layers of The Price Sandwich. None of those costs are optional, and none of them are inherently unfair.

What matters is whether you are paying a reasonable premium or an inflated one. Compare dealers on the same product, on the same day, using percentages above spot. Watch for red flags: “at spot” claims, call-for-price opacity, and aggressive steering toward high-premium coins. And remember that premiums are not fixed — they expand during crises and compress when supply is healthy. The patient buyer, the one who understands the Price Sandwich and shops accordingly, almost always pays less.

James Hartley

Former financial journalist (8 years) · Series 65 license holder

James covers retirement planning and precious metals investing. He spent eight years as a financial journalist before joining PrizeMining to research Gold IRA providers, fee structures, and regulatory requirements.

Sources

Gold IRA Due Diligence Checklist

10 items to verify before you open an account: fee transparency, custodian credentials, storage terms, buyback policies, and more. Free PDF, straight to your inbox.

No spam. Unsubscribe anytime. We never share your email.

This content is for informational purposes only and does not constitute financial, investment, or tax advice. Gold IRAs carry risks including price volatility, limited liquidity, and fees that can erode returns. Always consult a qualified financial advisor before making retirement investment decisions.